Availability prices for frequency control (FCR) and frequency restoration (aFRR/mFRR) have increased dramatically since the fourth quarter of 2020. This has caused a lot of interest in flexible generation and storage. Although the regulatory landscape is not optimal for storage assets, some larger scale storage projects are gaining momentum. Are these prices temporary or the start of a sustained trend? We will try to explain in this short article.

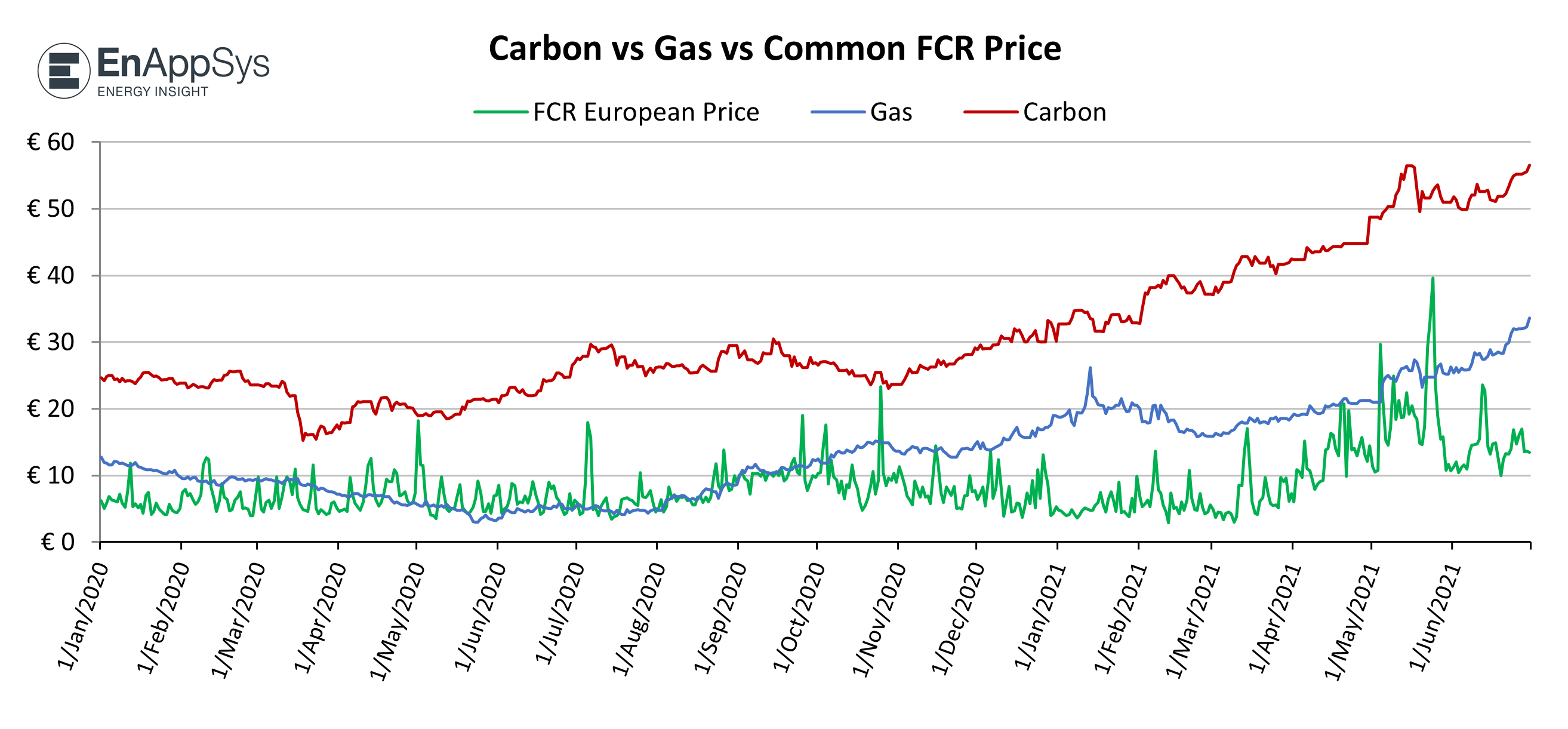

The main influence on these prices are gas and carbon prices. As this drives up the generation cost of conventional assets, these assets need to compensate for negative spark/dark spreads, by increasing their bids for availability on the reserve markets.

Ramp speeds and response times cannot be met by a ‘cold’ asset, which means that to provide reserves, some conventional assets will have to be running despite a negative spark/dark spread. The more renewables on the grid, the lower the day-ahead price will be and the larger the difference between marginal generation cost and day-ahead price.

Figure 1: Carbon vs Gas Common FCR Price

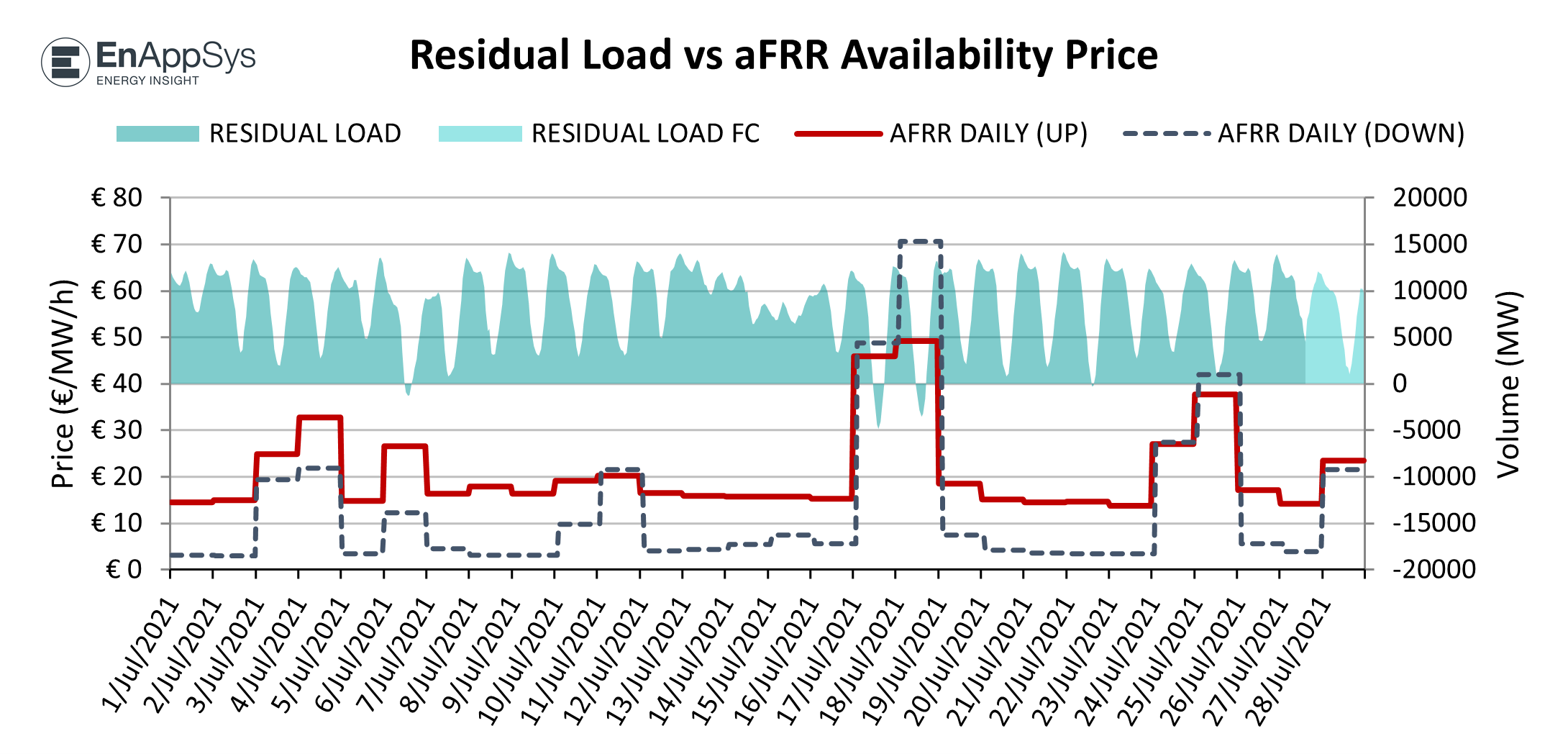

Another aspect is that while renewable generation increases, it will continue to push conventional generation out-of-merit for longer periods of time. We can see how this is already heavily impacting the weekends, where demand is lower. We sometimes see the residual load going negative during solar peak. Further growth will cause similar periods to occur during weekdays (figure 2).

Market rules have changed, reducing the length of the delivery periods to allow for more competition. This has resulted in less certain revenues from ancillary services for large power plants as they need to make sure their bids/offers are accepted across several delivery periods to avoid running at negative spreads for long periods or facing start-up costs if they cannot run profitably and are forced to switch off between accepted periods. This may impact bidding strategies as the uncertainty of running will impact both upward and downward capacity bids, the aggregate of the two may be higher than in the past as parties need to cover their opportunity cost on both sides, if they are bidding symmetrical capacity.

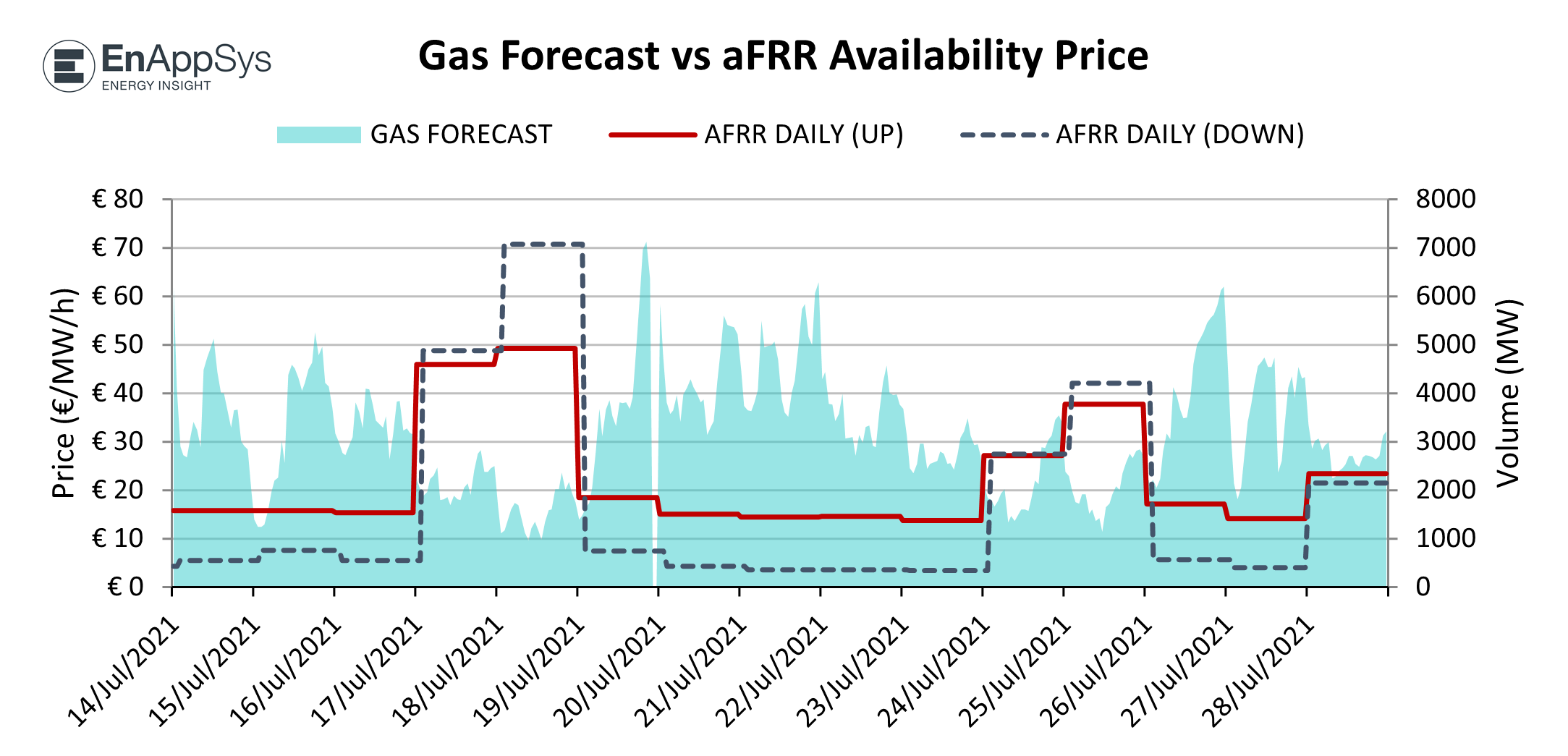

Where upward availability prices were traditionally higher than downward prices, in weekends we can see the reverse happening. Conventional plants will be running at minimum output, so they have very little downward flexibility. This introduces a scarcity aspect into the price (figure 3).

Figure 2: Residual Load vs aFRR Availability Price

Figure 3: Gas Forecast vs aFRR Availability Price

We see the high carbon prices as a given. After the rally started in April 2020 and saw corrections in May and June 2021, there seems to be a firm floor at € 50 per ton. With market experts expecting carbon prices between € 50 to € 80, or even € 100 in the medium term, there seems to be a strong case for enduring high availability prices. A drop in gas prices may temporarily reduce these prices, but with low storage levels for gas and no change in summer-winter price-spreads, low gas prices like we have seen in previous years are unlikely.

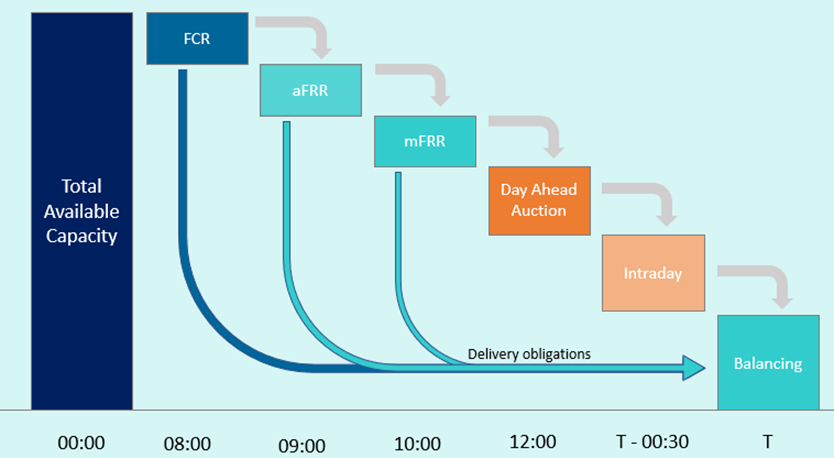

As long as conventional power is needed to balance the grid, it looks like the opportunity costs of these assets will set the price for availability fees. Flexible assets will look to optimize revenue by cascading their volume through a series of auctions.

The remaining volume can then be used for intraday optimization through the intraday exchanges or in the energy-only balancing market. Analysing these opportunities and improving insight into the fundamentals behind them will be crucial.

As flexibility will continue to become more important, having an insight into what drives availability prices and activation prices is essential for anyone having flexible assets, or trading the markets in which these assets play a major role.

Figure 4: Timeperiods Auctions

Optimise you revenues with over 60 unique charts

Set your pricing strategies more effectively

Analyse availability prices vs key drivers, such as margin, renewables, residual load and opportunity costs

Cascade flexible volume through the sequence of FCR, aFRR and mFRR auctions

If you would like to book a free trial or to arrange a demo so we can take you through the full range of functionality, please get in touch with our expert Jean-Paul Harreman and his team at

EnAppSys Ltd.

call +44 1642 671111

info@enappsys.com

Registered Office

EnAppSys Ltd, Blenheim House, Falcon Court, Stockton-on-Tees. Registered in England and Wales No. 4685938.