The Capacity Market is a mechanism introduced by the Government to ensure that electricity supply continues to meet demand as more volatile and unpredictable renewable generation plants come on stream. In the T-1 auction, potential Capacity Market participants can bid for contracts in auctions held one year ahead of the delivery date.

During the delivery year, capacity providers will receive monthly payments for their agreed obligation at the auction clearing price. Providers are expected to be available to respond with their agreed generation volumes or load reductions when called on by National Grid ESO at times of system stress.

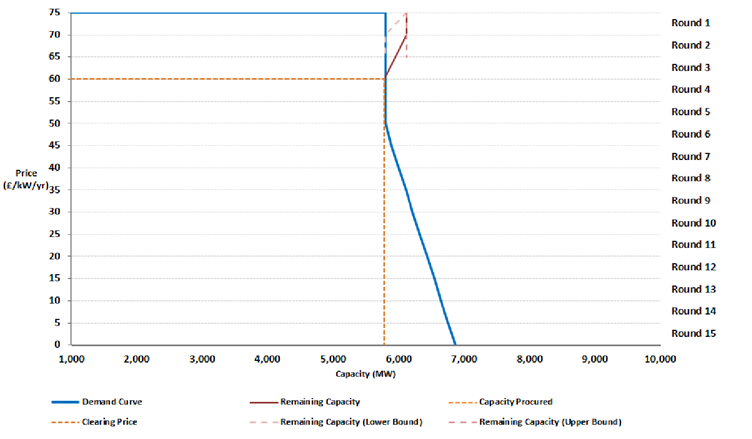

The auctions follow a descending clock format, starting with offers of £75/kW/year and gradually reducing until the minimum price is reached at which the supply of capacity offered by bidders is equal to the volume required.

The T-1 Capacity Market Auction for delivery year 2023/24 took place on 14th February 2023 and concluded at 11:30 after three rounds of bidding at a clearing price of £60/kW/year. A total of 6.1GW of derated capacity entered the auction against a target capacity of 5.8GW, the highest target capacity of any T-1 auction since the auctions began.

Such a high target capacity indicates that NG ESO is seeking to place further emphasis on domestic solutions to energy supply issues, something it demonstrated this winter with the Winter Contingency contracts that kept coal units in reserve that were otherwise set to be retired.

Due to the extreme market conditions seen in the last 18 months, and with NG ESO paying a premium for coal capacity under the Winter Contingency Contracts, capacity is far more highly valued than when the T-4 auction for the 2023-24 delivery year took place in March 2020. That auction cleared at £15.97/kW/year, around one quarter of the clearing price of this year’s T-1 auction, meaning that units that won a contract in this auction will receive approximately four times the payment for their capacity as units who won contracts in the T-4 for the same delivery year.

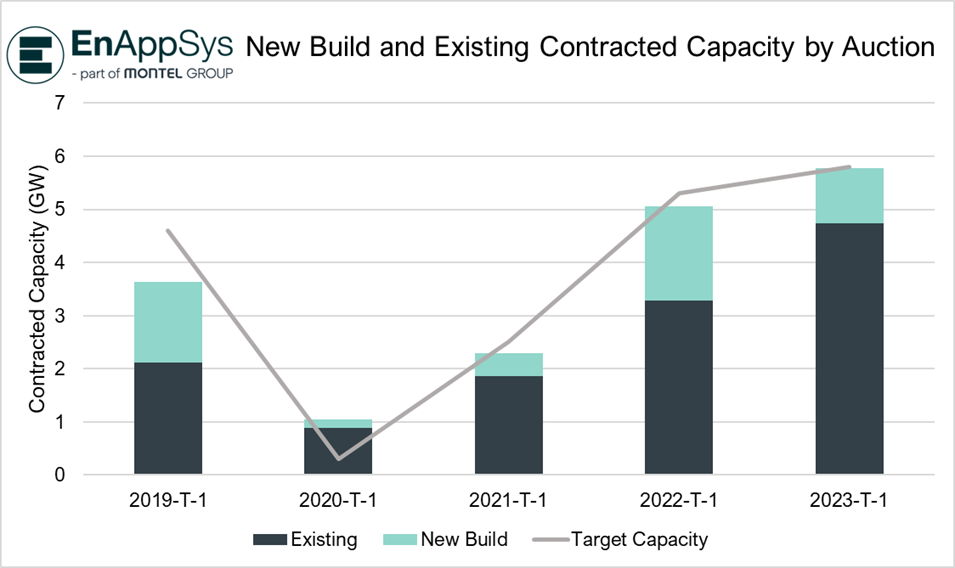

The high target capacity ensured that the marginal unit was a new build asset, as only 4.8GW of existing assets entered the auction, around 1GW less than the target. This was despite the entry of nuclear units into the T-1 auction for the first time, with Heysham 1 and Hartlepool 1 and 2 all winning contracts, resulting in this auction seeing more existing capacity win contracts than in any other T-1 auction.

The predominance of nuclear capacity in the auction resulted in a smaller amount of new build capacity entering than in the previous T-1 auction, with 1.0GW winning contracts against 1.7GW the year before. However, due to last year’s auction clearing at the maximum possible price of £75/kW/year, there has been a substantial increase in new build battery capacity in the action, with more than twice as much wining contracts as last year. Of the new build capacity than won contracts, 54% (568MW) was from batteries against just 15% (261MW) last year.

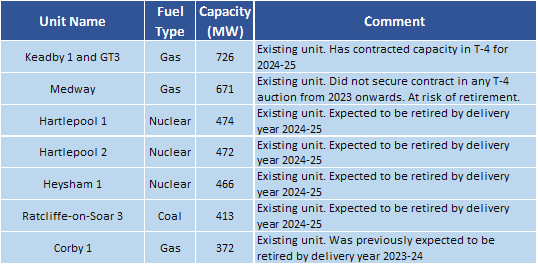

Among the largest units to win contracts in this year’s auction were Medway and Corby 1. These units were in risk of being retired as they have no contracted capacity beyond their new contracts gained in this auction. Corby 1 had previously opted-out of the T-4 auction for this delivery year as it was expected to be retired, but it has now contracted its capacity. These units will remain open for at least as long as these contracts apply, an example of how the high target capacity has placed emphasis on domestic generation. Keadby 1, the largest unit to win a contract this year, has been contracted in the T-4 auction for delivery year 2025-26 and so was not at risk of retirement.

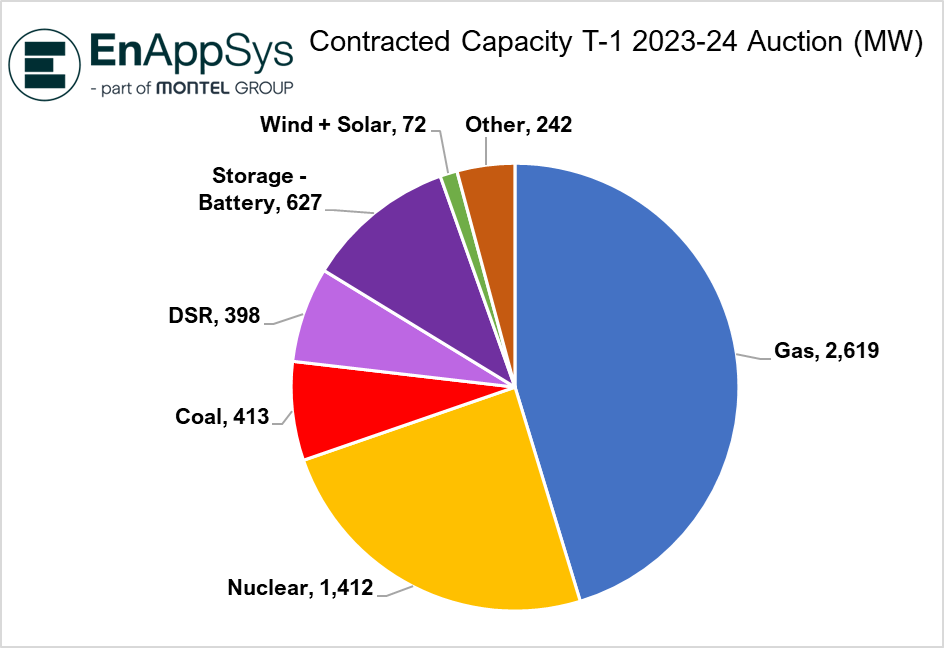

Ratcliffe-on-Soar 3 won a contract and was the only coal unit to do so. Each of the other Ratcliffe coal units had previously won a contract in the T-4 auction.

Over 65MW of wind capacity was contracted this year, the highest ever seen in a T-1 auction, beating the previous record of 14MW seen in the T-1 auction for delivery year 2021-22, further demonstrating the focus on domestic generation in ensuring stability.

EnAppSys director Phil Hewitt said “NG ESO have procured more capacity than ever before in a T-1 auction and the result is a high clearing price, though the price is likely cheaper than that of the Winter Contingency contracts seen this winter.”

“The key beneficiaries of this auction are the larger units Medway and Corby that did not secure contracts in the prior T-4 auctions but are being kept online by the prices in this T-1. It demonstrates that, going forward, NG ESO is keen to reduce their reliance on interconnectors and become more confident in their ability to resolve supply issues domestically.”

“Another stand out is that a coal power station unit slated to close has now extended its life for another year showing that coal is not dead … yet.”

New build-battery units have also benefitted from the higher prices, with more than half of the new build capacity that was awarded contracts being from batteries. Many of these units will see their start dates brought forward in order to make the most of the high clearing price.”

The units with the highest capacities that won contracts can be seen below along with some accompanying commentary.

EnAppSys Ltd.

call +44 1642 671111

info@enappsys.com

Registered Office

EnAppSys Ltd, Blenheim House, Falcon Court, Stockton-on-Tees. Registered in England and Wales No. 4685938.