National Grid ESO has announced two new services for Winter this year. The “Winter Demand Flexibility Service” is a first outing for domestic DSR and is an exciting development. The second service is the “Winter Contingency Service” which keeps some coal plant around for the winter with a unique system price innovation which will create generally higher prices when the plant is active in the BM.

This has come out of a pilot project carried out with Octopus Energy’s customers where they were asked to reduce their consumption during the evening peak. This resulted in an average demand response of 12.3MW at an average price of £227/MWh from 105,000 customers. If replicated across the whole consumer base (27m meters) this would equate to 3.1GW. So there is some potential for a significant response but it will not arrive for this tight winter. The price is also interesting as it is quite low meaning that potentially domestic DSR is a possible disruptor to conventional balancing service providers. If anything, consumers are under valuing their demand response.

It will be interesting how big this response would be in the winter and the price. It shows the power of domestic demand response (something EnAppSys has been working on with other suppliers on R&D projects) and the cost effectiveness of this kind of response for consumers. Some questions come to mind. If it became a regular event would the size of the response be as large, would crisis fatigue set in? Octopus customers are typically early adopters with some on flexible time of use tariffs so are not representative of the customer base as a whole so you can expect the response from the whole consumer fleet to not be proportionately as large.

For market participants, the new service will cause short term optimization issues. The new service will be accessed outside of the current Balancing Mechanism and Platform for Ancillary Services routes so any response will result in a reduction in demand and will later on come back into settlement as BSAD volumes. National Grid ESO needs to ensure that the market gets some real time visibility on the price and size of the response.

This is similar to the SBR service that was commissioned before the implementation of the capacity mechanism. This will keep on coal units from Drax and West Burton A with potentially a unit at Ratcliffe that was due to be decommissioned. The cost will be between £220m to £420m. There is a policy dimension to this, surely with a capacity mechanism there should be no risk to security of supply so the fact that additional capacity is having to be procured is a policy failure.

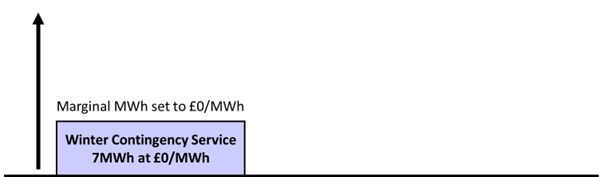

When the SBR service was used before the CM, if the SBR units were called, then the price in imbalance would have been at the VoLL at the time (i.e. £3,000/MWh). The market was assuming that this would be the case this time, that the units would be priced at VoLL, i.e. £6,000/MWh. Instead the price that has been chosen is £0/MWh but with a system flag. This at first seems counterintuitive but when you think about and run system pricing scenarios it is a sensible decision.

First we have to describe three features of the pricing algorithm, the first is NIV Tagging, the second is SO-Flagging and the final feature is Arbitrage Tagging.

One of the last steps of the Elexon imbalance pricing algorithm is NIV Tagging where the smaller stack (either the bid side or offer side and the being the non-price setting side) is subtracted from the larger stack, removing the most expensive actions from the price setting side.

If an action is SO-Flagged then it is unpriced if it is the most expensive action, it retains its price if there is a more expensive non-SO-Flagged action. This means that a zero priced system action will almost always retain its price unless there is an alternative energy action higher in the stack. If this is the case then it will be priced at the market index price.

If an action is Arbitrage Tagged then it means that there is an equivalent higher priced action on the other side of the system price algorithm. An example is that if NG ESO accepts offer of £100/MWh and accepts a bid of £120/MWh this is an arbitrage, they have sold at £120 and bought back at £100. In this case with a price for the offer of £0/MWh and almost every action on the bid side being at a price of more than £0/MWh the volume of the action will be arbitraged away and the volume will cancel actions on the bid side. This will result in a reduction in actions and volumes on both the bid and offer side.

There has been some breathless excitement in the industry of the effect of a zero price for an action and the potential ability for a zero price for power when the system is short because the winter contingency power plants will be setting the price.

There is a very, very, very unlikely edge case where a short system could have a price of zero but this is unlikely. Let us explain with some examples. In these examples we will use the colour coding from the Elexon imbalance pricing document at https://www.elexon.co.uk/documents/training-guidance/bsc-guidance-notes/imbalance-pricing/.

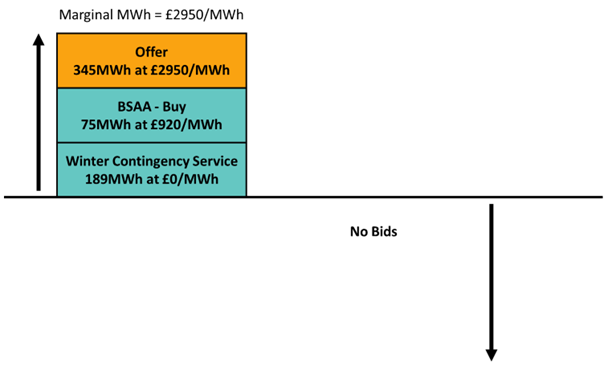

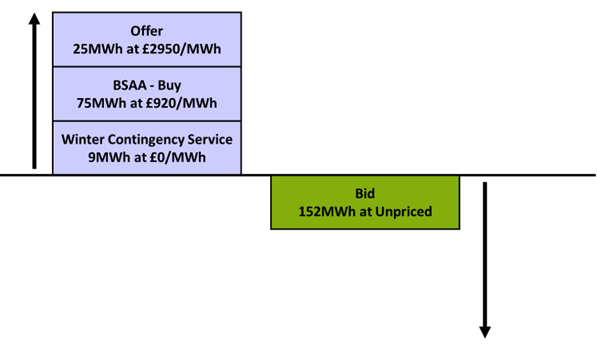

In this scenario NG ESO has activated the winter contingency service, a system buy interconnector trade at £920/MWh and an energy offer in the BM for £2950/MWh. There are no actions on the bid side so the system imbalance price is just the energy offer in the BM for £2950/MWh.

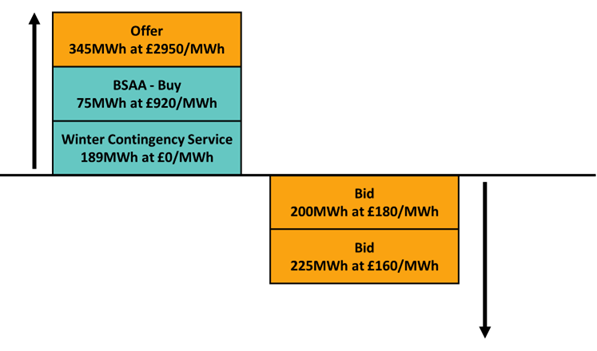

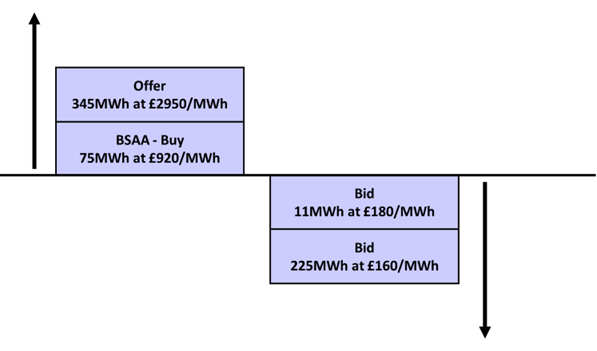

In this scenario NG ESO has activated the winter contingency service, a system buy interconnector trade at £920/MWh and an energy offer in the BM for £2950/MWh. There are actions on the bid side at £180/MWh and £160/MWh.

Because the winter contingency service action is priced at £0/MWh and the actions on the bid side do not NIV tag the volume from the top as some might think initially but because of arbitrage tagging they remove the winter contingency service action first reducing the size of the bid side from the bottom.

In this case with the smaller bid side stack this is then NIV tagged from the top of the offer side resulting in the same marginal price as before £2950/MWh not a price of £0/MWh.

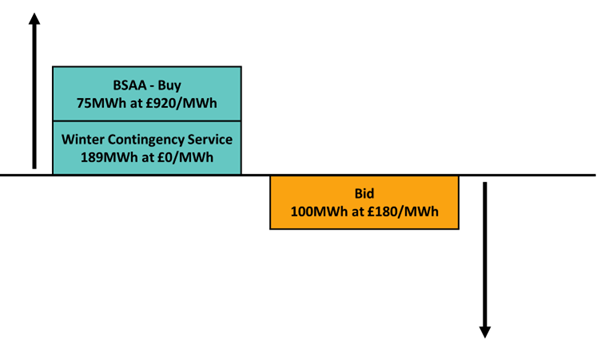

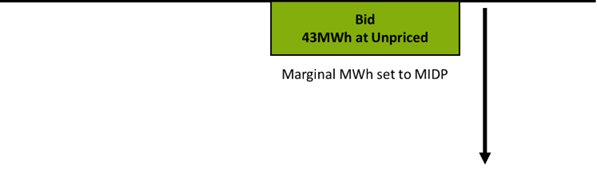

In this scenario NG ESO has activated the winter contingency service and a system buy interconnector trade at £920/MWh. There is a bid action that is priced above the winter contingency service.

In this case the arbitrage happens again and the remaining actions, as they are all system actions, become unpriced in second stage flagging and then set the imbalance price to the MIDP as there is no price in the stack.

In this scenario NG ESO has activated the winter contingency service, a system buy interconnector trade at £920/MWh and an energy offer in the BM for £2950/MWh. There are actions on the bid side at £180/MWh and a system action of -£57/MWh from a windfarm being bid off for constraints.

In this case the arbitrage happens again, the system actions on the buy side all keep their price because there is a more expensive energy action but there is a little bit of the zero priced winter contingency action left after the arbitrage. The bid side is then left as the second stage flagged wind constraint action as it is more expensive than the winter contingency action.

In this case the NIV tagging then results with a small amount of the winter contingency left and the imbalance price is set to zero.

However, this is a very unlikely situation for which the following have to be true:

1. The size of the positively priced bid stack has to be less than the size of the winter contingency action

2. The grid has to be turning off windfarms in a situation when the system is very short of margin so has to switch on the winter contingency, this is unlikely to occur as the margin issue will be due to low wind generation

3. The size of the remaining bid stack then has to be not large enough to not flip the system short but not large enough to remove all other actions from the stack except for the winter contingency action, again unlikely.

It is safe to say this edge case scenario whilst mathematically possible is very unlikely.

In this scenario NG ESO has activated the winter contingency service, a system buy interconnector trade at £920/MWh and a small energy offer in the BM for £2950/MWh. There are actions on the bid side at £180/MWh and a system action of -£57/MWh from a windfarm being bid off for constraints.

As in many previous cases, in this case the arbitrage happens again, the system actions on the buy side all keep their price because there is a more expensive energy action but there is a little bit of the zero priced winter contingency action left after the arbitrage. Again, the bid side is then left as the second stage flagged wind constraint action as it is more expensive than the winter contingency action.

Finally as the bid stack is larger than the offer stack the bid side sets the imbalance price with the remaining action being unpriced so set to the market index price.

At first glance, an action in the offer pricing stack at a price of zero feels like it will result in imbalance prices going to zero if the NIV is small but positive. This is incorrect because arbitrage tagging will remove the winter contingency action from offer stack and it will never set the price except in exceptional and very unlikely circumstances.

The effect of this pricing approach means that it will typically reduce the size of the bid stack in any stress periods activating more of the highest price actions in the offer stack making prices more expensive in a short system encouraging more response. This is generally a good thing.

EnAppSys Ltd.

call +44 1642 671111

info@enappsys.com

Registered Office

EnAppSys Ltd, Blenheim House, Falcon Court, Stockton-on-Tees. Registered in England and Wales No. 4685938.