The Capacity Market is a mechanism introduced by the Government to ensure that electricity supply continues to meet demand as more intermittent and unpredictable renewable generation plants come on stream. In the T-1 auction, potential Capacity Market participants can bid for contracts in auctions held one year ahead of the delivery date.

During the delivery year, capacity providers will receive monthly payments for their agreed obligation at the auction clearing price. Providers are expected to be available to respond with their agreed generation volumes or load reductions when called on by National Grid at times of system stress.

The auctions follow a descending clock format, starting with offers of £75/kW/year and reducing incrementally in subsequent rounds until the minimum price is reached at which the supply of capacity offered by bidders is equal to the volume required.

The T-1 Capacity Market Auction for delivery year 2022/23 took place on 15th February 2022 and concluded at 10:00 after a single round of bidding. A total of 4.996GW derated capacity had prequalified for the auction against a target capacity of 5.361GW.

Since the total prequalified derated capacity was less than the target capacity, all prequalified units won a contract at the price cap of £75/kW/year. The highest clearing price in any Capacity Market auction until now had been £45/kW/year – seen in the previous T-1 auction and itself double the previous high of £22.50/kW/yr set in the T-4 auction for 2020/21 delivery.

This came following a year of extreme market conditions, preceded by the loss of three large gas-fired power stations owned by Calon Energy when this power station operator went into administration. After this event, these plants withdrew from the power market, reducing capacity margins for winter 2021/22, and have not been allowed to participate in Capacity Market auctions since.

One of these power stations, Baglan Bay, had previously not taken capacity contracts for delivery in 2022/23 and was unable to re-enter the auction this time around which decreased the prequalified capacity by ~0.5GW.

Meanwhile, other units, Severn Power and Sutton Bridge, had their contracts from the T-3 auction for delivery year 2022-23 terminated. This increased the target capacity of the T-1 auction by ~2GW as a replacement for the lost capacity.

The loss of these three plants was highly significant in driving up the prices in this auction by increasing the demand for capacity and decreasing supply.

The beneficiaries were the units that had not already taken capacity contracts for the delivery year but which were able to provide capacity at this short notice, with units earning around twelve times more for their capacity than those in the T-3 auction. The prior T-3 auction for the same delivery year cleared at £6.44/kW/year.

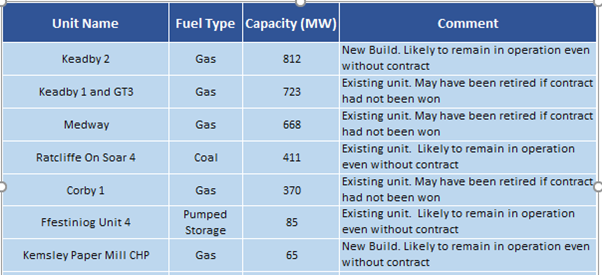

Among the beneficiaries were some large units that otherwise risked being retired which have been kept online by this latest auction, such as Keadby 1, Medway and Corby 1 which have a collective capacity of ~1.7GW.

These additional units remaining in operation for the near-future is likely to contribute towards a more stable system after the loss of three large units last winter, with units being incentivised to provide capacity in times of system stress that would otherwise have not been operational.

Sixty three new build Capacity Market Units also won contracts in this auction with a combined capacity of ~1.4GW – a record high for new builds in the T-1 auctions. This is largely the result of 811MW Keadby 2 unit, the largest unit to win a contract in the auction, which comprised more than half of the new build capacity.

The units with the highest capacities that won contracts can be seen below along with some accompanying commentary.

EnAppSys Ltd.

call +44 1642 671111

info@enappsys.com

Registered Office

EnAppSys Ltd, Blenheim House, Falcon Court, Stockton-on-Tees. Registered in England and Wales No. 4685938.