Owners of peaking assets have cashed in on higher prices and revenue-generating opportunities following the launch of STOR (Short-Term Operating Reserve) as a day-ahead service.

STOR was re-introduced on April 1 and unlike its previous incarnation, which was tendered for season-long durations, the new replacement service is based on daily auctions – giving providers the flexibility to optimise on a daily basis between STOR and other market segments.

National Grid ESO began procuring STOR on a rolling daily basis from April 1, with a target requirement for 1,310MW holding capacity. The capacity is procured via a daily auction held before the day-ahead EPEX and Nordpool auctions in the wholesale energy market.

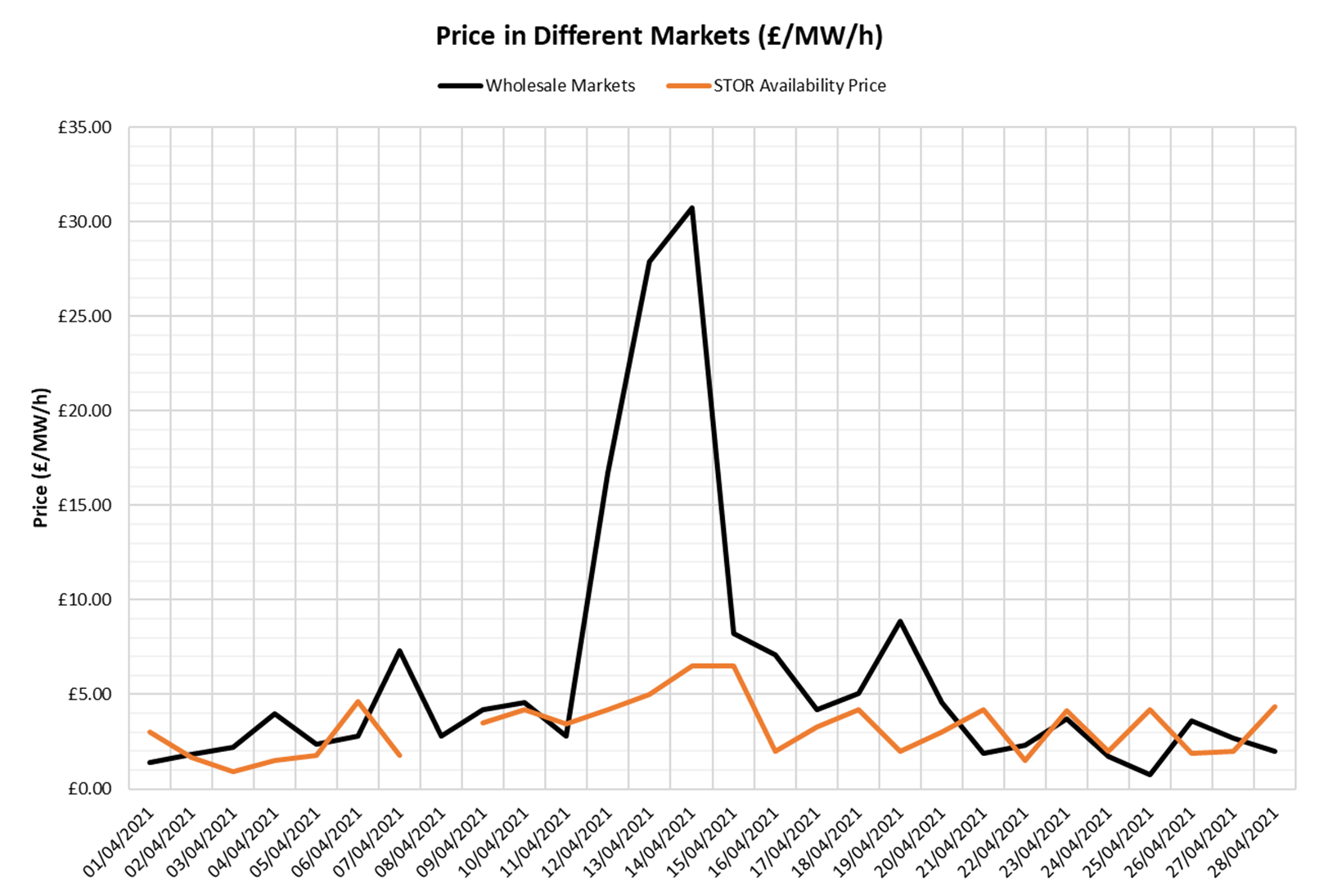

During STOR’s first month of operation, holding (availability) prices ranging from £0.50/MW/h to £6.50/MW/h and averaging around £3.00/MW/h were paid. These prices were generally higher than those in the same period in both 2019 and 2020.

The relaunch of STOR as a day-ahead service has provided opportunities for savvy operators to make money.

Following the tight system and high prices seen in the energy market on 12 April, STOR prices rose in subsequent days as providers of capacity factored in the expected value of lost opportunity in the energy market. On that day, cash-out prices reached £1,971.59/MWh and STOR providers on subsequent days sought increased fees to cover the opportunity cost that resulted from not participating in the energy markets.

Effectively, STOR’s return as a day-ahead service is part of National Grid’s plan to move procurement of grid services closer to real time. Participants in this service are able opt in and out of this segment of the market on a daily basis as the prevailing economics dictate, and can optimise against other revenues available in the wholesale markets and/or balancing mechanism.

To succeed in this more dynamic market environment, participants will need tools and systems to actively monitor and forecast all market segments and to optimise between them on a daily basis.

At the beginning of April there was a high volume offered into the STOR market (2,918MW on April 1), before gradually decreasing to 1,220MW on April 15, lower than the target requirement. Offered volumes stabilised in the second half of the month at around 2,000MW. Accepted volumes have ranged between 1,127MW and 1,313MW (excluding April 8 when a system glitch saw no tenders accepted).

There were cases of companies tendering in different units at different prices to test bidding strategies. For example, Uniper priced Killingholme 2-1 low at around £0.50/MW/h on most days, while pricing Killingholme 2-2 at around £1.25/MW/h. As a result, 2-1 was usually accepted, while 2-2 was usually rejected, entering the balancing mechanism instead.

As shown by the following chart, a unit generating in the wholesale market in April 2021 could have made between £0.80/MW/h and £30.70/MW/h equivalent, at an average of £5.90/MW/h.

When looking only at availability prices for STOR, during this period the wholesale market looked more favourable than STOR for the majority of days. However, the inclusion of any net income from utilisation prices, the details of which are not yet publicly available, may close the gap. Even if this is not taken into account, two days in April are still more favourable to STOR on availability price alone.

The chart shows expected revenues for a 40% efficient peaking unit derived using EnAppSys’ proprietary tools for unit benchmarking and expressed as £/MW/h equivalent for each day:

As a Reserve service, STOR provides volumes of active power (or demand reduction) into the system to help balance generation with demand, in the event of unforeseen deficits in generation. These deficits may result from sudden generation unavailability (such as a unit trip) or outturn generation being lower than forecast (such as wind out-turning low). STOR is one component of the Reserve held by National Grid, to ensure volumes are available to be called upon when needed.

Both Balancing Mechanism (BM) and non-BM units may provide STOR. BM STOR is activated through the balancing mechanism whilst non-BM STOR is activated through National Grid’s Platform for Ancillary Services (PAS).

Our Ancillary Services platform is now providing insight into the Short-Term Operating Reserve (STOR) service.

Quickly perform your own analysis to identify different trading strategies within the STOR market over time using historic data from 2013 to the present. Create custom dashboards to spot opportunities and pinpoint risks within the Ancillary Service market.

Get in contact now to optimise your revenue streams between STOR and other market segments.

EnAppSys Ltd.

call +44 1642 671111

info@enappsys.com

Registered Office

EnAppSys Ltd, Blenheim House, Falcon Court, Stockton-on-Tees. Registered in England and Wales No. 4685938.