The Capacity Market is a mechanism introduced by the Government with effect from Delivery Year 2018 to ensure that electricity generation capacity continues to meet peak demand as more volatile and unpredictable renewable generation plants come on stream. In the T-4 auction each year2, potential Capacity Market participants can bid for contracts in auctions held four years ahead of the delivery date.

During the delivery year, capacity providers receive monthly payments for their contracted obligation at the auction clearing price. Providers are expected to be available to respond with their agreed generation volumes or load reductions when called on by National Grid at times of system stress.

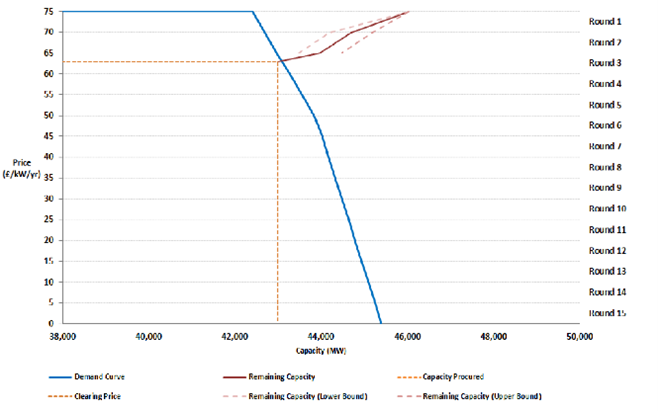

The auctions follow a descending clock format, starting with offers of £75/kW/year and gradually reducing on the basis of bidders’ submitted exit prices until the minimum price is reached at which the supply of capacity offered by bidders is equal to the volume required.

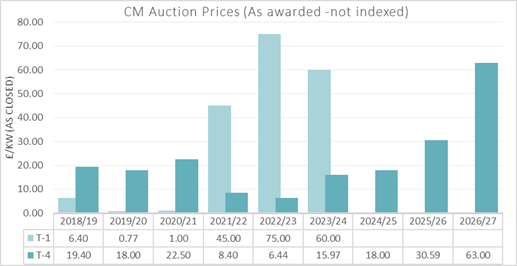

The T-4 Capacity Market Auction for delivery year 2026/27 took place on 21st February 2023 and concluded before noon after three rounds of bidding. A total of 46.0GW derated capacity had prequalified for the auction against a target capacity of 43.9GW and the auction cleared at the record-breaking price of £63/kW/year with 43GW of capacity-securing contracts, 12.5% of which were new-build3. EnAppSys director Phil Hewitt said, “If you won a contract this year certainly time to break out the bubbly!!!”

The reason for the record-breaking price is due to both a record-low prequalifying capacity as well as a higher capacity targeted by NG ESO.

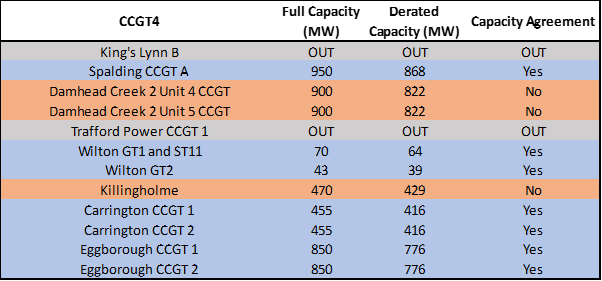

The original target as per the July 2022 report had been set at 42.4GW of derated capacity, which was 0.3GW higher than in the previous T-4 auction. In January, an adjustment to the target was proposed and accepted and an uplifted derated capacity target of 43.9GW was set. The magnitude of this shift matches the capacity of the gas units Eggborough CCGT Units 1 and 2 that won long-term fifteen-year contracts for the first time, which otherwise have a history of applying and not prequalifying in the previous three years.

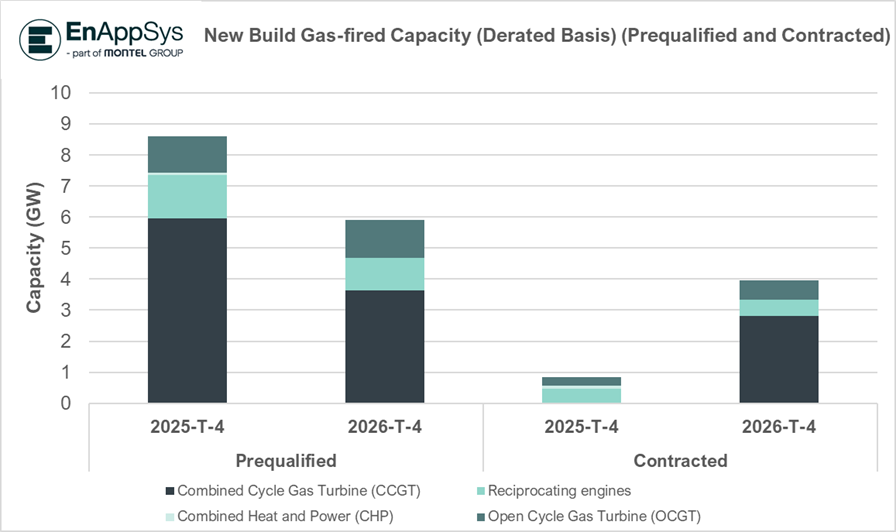

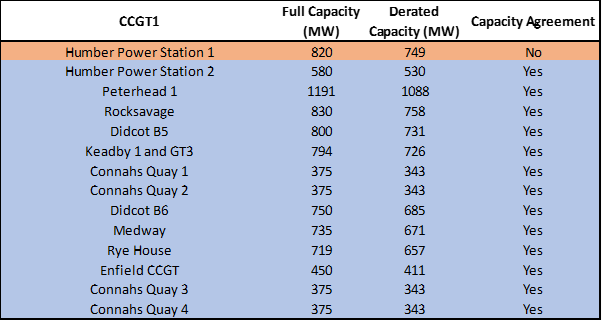

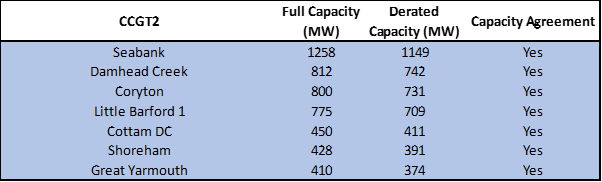

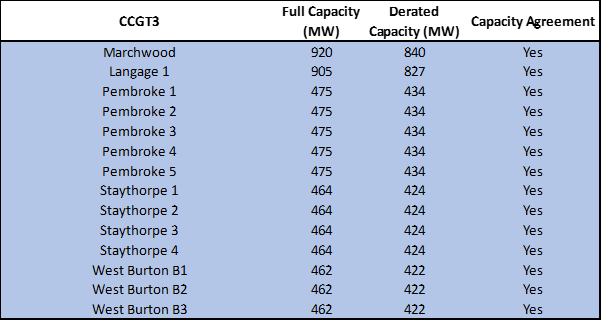

The new-build derated capacity that prequalified this year was low at 7.5GW, 3GW less than in the previous year’s auction. Around 5.3GW of this new-build derated capacity was accepted, 3.5GW of which were generating CMUs, with the balance comprised of 1.0GW interconnectors and 0.8GW DSR. Around 40% less new-build gas capacity was prequalified for this auction compared to the previous T-4 auction. Despite this, 2GW+ of new-build gas capacity was accepted which is more than double the new-build gas capacity accepted in the previous T-4 auction. Around 70% of the new build gas capacity arose from CCGT Eggborough Units 1 and 2. We can see this year-on-year difference in prequalified versus contracted gas capacity as well as the predominance of CCGT contracts over other gas types in the visualisation below.

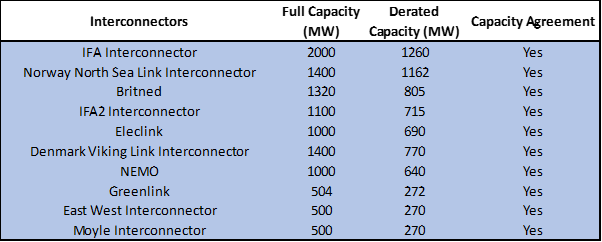

The next greatest contributions to contracted new-build capacity was from the Viking and the Greenlink interconnectors that each won one-year contracts with 0.8GW and 0.3GW derated capacity respectively. These were the only two new interconnectors. This is the third T-4 auction in a row in which the Viking interconnector has won a one-year contract and the first time Greenlink tendered.

Offshore wind and solar CMUs prequalified and were successful in securing capacity, which was not noted in the previous year.

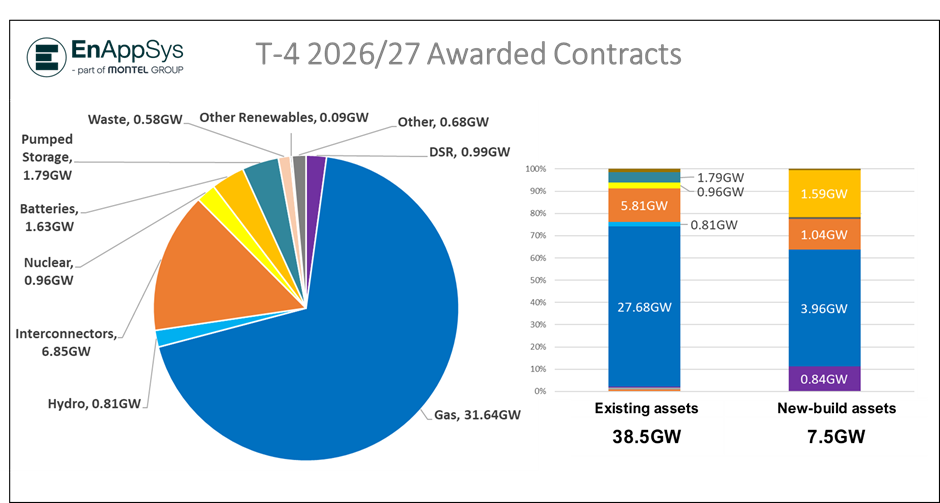

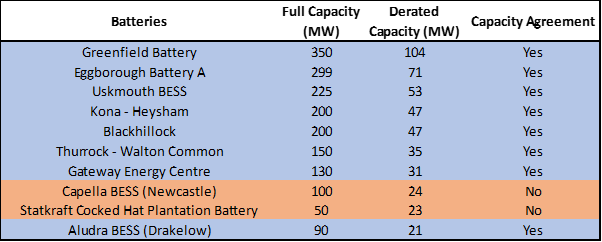

After gas, the second-largest contribution to contracted capacity by new-build fuel type was from batteries, with the auction procuring 1.25GW of derated capacity across 124 assets. This is an increase from the previous year, which saw ~1 GW of capacity across 89 assets. The new-build batteries that got accepted this year will provide a nominal capacity of over 5GW.

Around four-fifths of the batteries that won agreements had their capacity contracted for fifteen years – highly significant for them given the high clearing price.

Although technology agnostic4, the Capacity Market has secured significant battery storage capacity which supports the GB system’s growing reliance on less predictable renewable energy sources such as wind. To fulfil system demand during the times when renewable energy is low, more storage is needed as more renewable generation is build.

The breakdown on a derated capacity basis is shown in the chart below.

The same nuclear units Sizewell B Power Stations 1 and 2 secured contracts. These units are due to end generation in 2035.

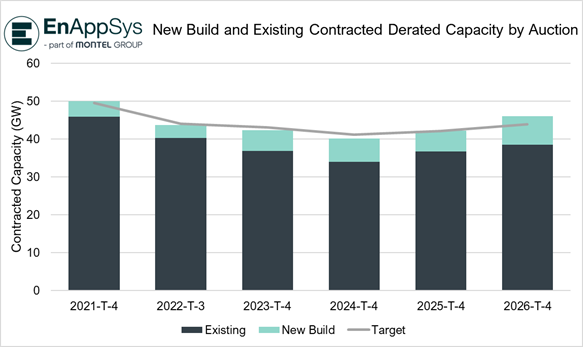

Interconnector units North Sea Link and Eleclink secured contracts this year under the category of existing assets for the first time. They previously secured contracts in the previous three T-4 auctions under the new-build assets category. The chart below shows the volume of new build and existing assets by auction. We can see a higher volume of existing assets this year, which arose from the category shift of these two interconnectors.

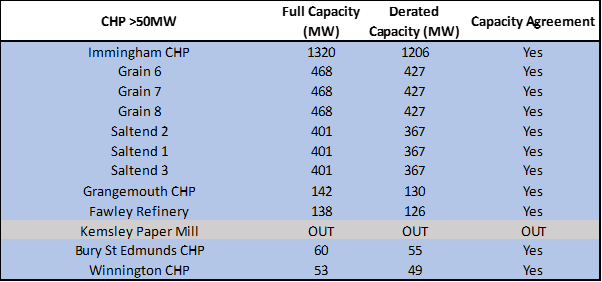

Most existing gas-fired units that won contracts in the previous year won contracts this year and all GB coal units are expected to phase out by the end of 2024 and none have participated in Capacity Market auctions since the T-4 delivery year of 2023-24.

![]()

Footnotes

1De-rating means that the supply is adjusted to take account of the availability of plant, specific to each type of generation technology.

2A further auction is then held one year ahead of the delivery year for additional capacity (the T-1 auction).

3New build assets are able to bid for multi-year contracts up to 15yrs in duration (subject to meeting specified cost threshold criteria) whereas existing assets (i.e. units currently in operation) are limited to contracts of 1yr duration.

4Although the CM applies different derating factors by technology class, the auction itself procures derated capacity solely on the basis of price.

EnAppSys Ltd.

call +44 1642 671111

info@enappsys.com

Registered Office

EnAppSys Ltd, Blenheim House, Falcon Court, Stockton-on-Tees. Registered in England and Wales No. 4685938.